For the past four years, thousands of Rawalpindi and Islamabad plot holders have been paying to own land they weren’t even using. A file sitting idle in a drawer still generated a tax bill every single year. That era is now over. With the Finance Act, 2026 effective from 1 July 2026, the notorious Section 7E “deemed income” tax has been struck from the Income Tax Ordinance, 2001 — and it lands on top of the earlier removal of the 3–7% Federal Excise Duty (FED) on property transfers. Together, these two changes remove a recurring annual holding cost and slash the friction of exiting a position. This is arguably the most investor-friendly shift the twin-cities plot market has seen in years.

What Exactly Was Section 7E?

Section 7E was inserted through the Finance Act, 2022. It taxed the deemed (notional, assumed) rental income of capital assets held as immovable property. In practice, resident individuals whose total qualifying properties exceeded a fair-market value of PKR 25 million were treated as if the property earned 5% of its value in rent, taxed at 20% — an effective charge of roughly 1% of fair market value, every year, whether the plot earned a single rupee or not.

The killer detail for investors: this applied to bare, non-productive plots and second homes. A vacant file generating zero cash flow still triggered an annual liability, and — critically — an FBR Section 7E certificate became a gatekeeping document required before you could register a sale. No certificate, no transfer. That single requirement froze liquidity across the market.

Why It Was Abolished

In May 2026, the Federal Constitutional Court of Pakistan (FCC) unanimously declared Section 7E unconstitutional and void from inception, holding that the federation cannot tax notional or “deemed” income where no actual income exists. The government then formally omitted the section in the Finance Act, 2026, effective 1 July 2026. The practical result: the levy is dead, pending Section 7E notices lose their force, and the certificate roadblock at the registrar’s office is removed.

The Two-Layer Relief, In Plain Numbers

It helps to separate the two reforms, because they arrived a year apart and do different jobs. The 7% FED was a one-time transaction cost on transfers; the 1% Section 7E was a recurring annual holding cost.

| Tax | What it hit | Old cost | Status now |

|---|---|---|---|

| Section 7E (deemed income) | Idle plots / second homes over PKR 25m FMV — annually | ~1% of FMV per year | Abolished from 1 July 2026 |

| Federal Excise Duty (FED) | Transfer of plots, houses, commercial units | 3% filer / 5% late filer / 7% non-filer | Removed (Budget 2025–26) |

| Advance tax on seller (236C) | Seller at transfer | 4.5%–5.5% | Cut to flat 2.75% (ATL) |

| Advance tax on buyer (236K) | Buyer at purchase | 1.5%–2.5% | Cut to flat 1.25% (ATL) |

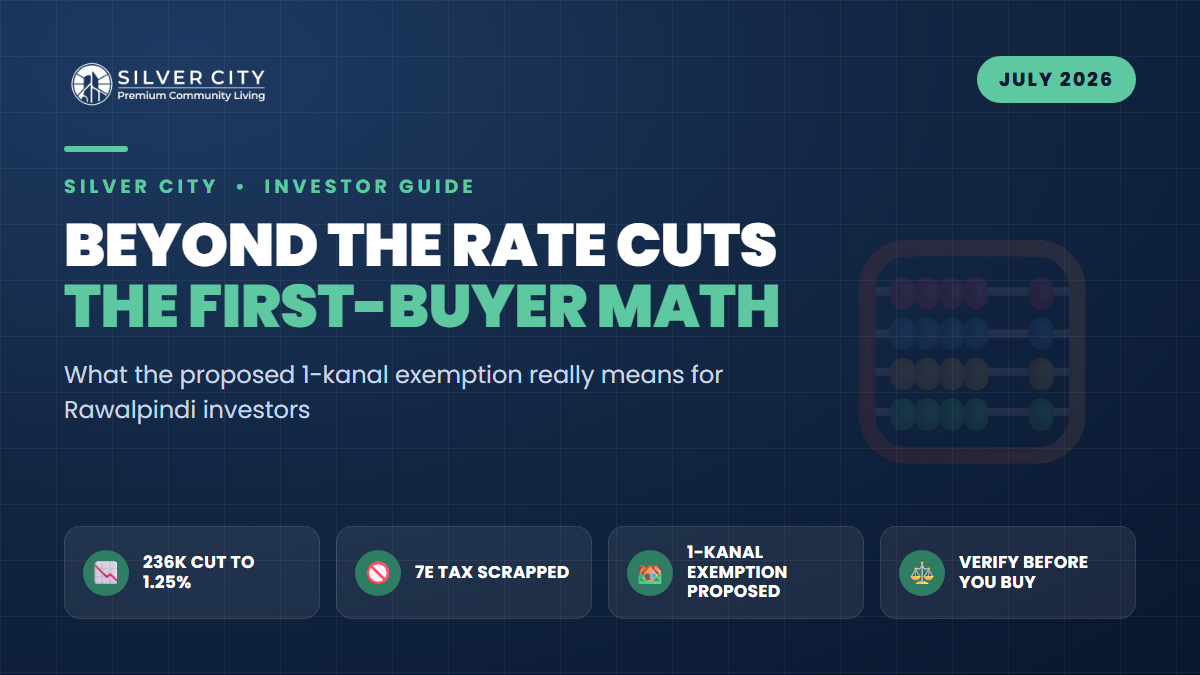

A Worked Example

Suppose you hold a 1 Kanal file with a fair-market value of PKR 30 million that you bought as a hold-and-flip and never developed.

- Under the old regime: Section 7E cost you roughly PKR 300,000 every year just to keep it, plus you needed a 7E certificate before selling — and a buyer faced 7% FED on transfer.

- From July 2026: that PKR 300,000 annual bleed is zero, no certificate is required to register the sale, and the transfer-side FED is gone. Combined seller-plus-buyer advance tax has also roughly halved.

Over a typical 3–4 year hold, that is close to PKR 1 million of holding tax that simply disappears — money that previously ate directly into capital gains.

Why This Unlocks Liquidity For “Idle File” Investors

The twin-cities market had quietly seized up. Many investors were stuck: unwilling to keep paying 7E on a non-earning asset, yet unable to sell smoothly because the certificate process and layered transfer taxes scared off buyers and shrank the buyer pool. That gridlock is what these repeals break.

- No annual carrying cost. A plot can now be held patiently without an annual tax penalty, so there is no forced-sale pressure and no reason to dump files below market.

- Cleaner, faster transfers. Removing the 7E certificate requirement and the FED strips out paperwork and cost at the registrar, shortening deal timelines.

- A wider buyer pool. Lower buyer-side tax (236K at 1.25% for filers) brings hesitant, price-sensitive buyers back — the exact demand a seller needs to convert an idle file into cash.

- Better net returns. With holding and transaction taxes gone, more of any price appreciation stays with the investor.

Timeline At A Glance

| When | Event |

|---|---|

| Finance Act 2022 | Section 7E introduced (1% deemed tax) |

| Budget 2025–26 | 3–7% FED on property transfers abolished |

| May 2026 | FCC declares Section 7E unconstitutional |

| 1 July 2026 | Section 7E formally omitted; 236C/236K rates cut |

What Smart Investors Should Do Now

- Re-price your idle files. Rework your net-return maths without the annual 7E drag — many “dead” holdings are now viable to keep or profitably sell.

- Stay on the Active Taxpayers List (ATL). The best 236C/236K rates apply only to filers; non-filers still pay materially more and face restrictions.

- Confirm registrar practice locally. Because the change is fresh, verify with your society office and sub-registrar that the 7E certificate is no longer being demanded before you finalise a transfer.

- Target genuinely approved projects. Tax relief widens demand for secure, litigation-free land — approval status matters more than ever.

Frequently Asked Questions

Do I still need an FBR Section 7E certificate to sell my plot?

With Section 7E omitted from the Ordinance effective 1 July 2026 and struck down by the Federal Constitutional Court, the legal basis for demanding the certificate is gone. In practice, confirm with your local sub-registrar and society office, as field procedures can take a short while to catch up with the law.

Was the 7% FED and Section 7E abolished at the same time?

No — they were two separate steps. The 3–7% Federal Excise Duty on property transfers was removed in the 2025–26 budget, while Section 7E was formally abolished a year later, effective 1 July 2026. The combined effect is what investors are feeling now.

I paid Section 7E in earlier years — can I claim it back?

The court held the levy void from inception, which strengthens taxpayers’ position on past demands and pending notices. Refunds and adjustments of already-paid amounts depend on your specific assessment and FBR/court guidance, so consult a qualified tax advisor before filing any claim.

Does removing these taxes mean plot prices will rise?

Lower holding and transaction costs typically widen the buyer pool and improve liquidity, which supports prices — especially in approved, well-located projects. It is a positive demand signal, not a guarantee; location, approval status and developer track record still drive real returns.

The Bottom Line

The abolition of Section 7E, layered on the earlier removal of the FED and the halving of transfer taxes, rewrites the maths for anyone holding idle plot files in Rawalpindi. Zero annual deemed tax plus a cleaner exit means capital that was trapped can finally move. In this friendlier environment, the smart play is approved, secure land — which is why an RDA-approved society like Silver City on Girja Road near the Thalian Interchange, with residential options from 3.5 Marla to 1 Kanal and structured installment plans, is well worth considering as you redeploy freed-up capital into a documented, low-risk asset.