For nearly a decade, the story of real estate around Rawalpindi’s western belt has been a story about roads. The Rawalpindi Ring Road, its interchanges at Adiala and Chakri, and the promise of a fast link to the M-2 Motorway did the heavy lifting on land values. That first chapter is closing. Under CPEC 2.0, the national conversation has moved from building infrastructure to filling it with industry — and that shift is the catalyst serious investors near Adiala and Chakri should be watching in 2026.

What Actually Changed: CPEC Phase 2.0

The headline number is real. Pakistan’s Special Economic Zones expanded from 7 in 2019 to 44 by 2025, after 37 new zones were notified through the Board of Investment. But the count matters less than the change in philosophy. CPEC Phase 1 created zones that were often little more than lines on a map — administrative designations with no power, water, or road connectivity behind them.

CPEC 2.0 reverses that sequence. The official Long-Term Plan for industrial cooperation now emphasises industry-led growth, export-oriented manufacturing, technology transfer and value addition, with SEZs positioned as anchor platforms rather than tax gimmicks. Priority zones such as Rashakai (KP), Dhabeji (Sindh), Bostan (Pishin) and Allama Iqbal Industrial City near Faisalabad are being connected to utilities before being pitched to investors. Allama Iqbal Industrial City had reportedly reached roughly 73% occupancy by 2025 — proof that when the plumbing exists, factories follow.

The Local Trigger: A PIEDMC Estate on the Ring Road

The Pindi-specific version of this shift arrived in 2026. The Punjab Industrial Estates Development and Management Company (PIEDMC) approved an industrial estate alongside the Rawalpindi Ring Road, replacing an earlier Special Economic Zone proposal for the same corridor.

Why the switch from SEZ to industrial estate? It is a direct consequence of Pakistan’s IMF programme. Under the current arrangement, the tax exemptions and incentive packages that legally define an SEZ cannot be extended. The industrial estate model requires no such exemptions, which is precisely why it cleared PIEDMC’s board while the SEZ did not. Land would be acquired and offered to industrial investors at affordable rates.

Be clear-eyed about the stage, however. As of mid-2026 the Punjab Assembly has not yet passed the enabling legislation, land acquisition has not started, and no plots are open for application. This is an approved plan with real momentum — not a shovel in the ground. Treat it as a forward indicator, not a completed asset.

Why Industry Reprices Land Differently Than Roads

Infrastructure and industry drive value through different mechanisms, and the second is stickier than the first:

- Roads create access; factories create demand. An interchange shortens your commute. An industrial estate creates thousands of jobs, and those workers need housing, rentals, shops and services nearby.

- Industry anchors end-users, not just speculators. Road-driven booms attract flippers. Employment-driven demand brings families who buy to live, which deepens and stabilises a market.

- Rental yield turns on. Salaried industrial workers are the tenant base that transforms a plot-only society into a functioning neighbourhood with recurring rental income.

- Commercial multiplier. Estates pull logistics, warehousing and small manufacturing, lifting commercial plot values along the feeder roads.

The Adiala and Chakri Corridors: What the Numbers Say

The Rawalpindi Ring Road is a roughly 38–40 km, six-lane corridor linking GT Road near Rawat to the Thalian Interchange by Islamabad Airport, with major interchanges at Banth, Chak Beli Khan, Adiala and Chakri reported complete or near-complete. Property along the corridor has already appreciated in the range of 20–40% over recent years.

The Chakri interchange is widely regarded as the corridor’s strongest real-estate node because it offers direct access to the M-2 Motorway plus quick links into both Rawalpindi and Islamabad. Adiala anchors the second major cluster of housing-society activity. The table below frames how the value catalyst is evolving.

| Driver | Phase 1 (2018–2025) | Phase 2 (2026 onward) |

|---|---|---|

| Primary catalyst | Ring Road + interchanges | PIEDMC industrial estate + CPEC 2.0 industry |

| Value mechanism | Access & connectivity | Jobs, tenants, commercial demand |

| Buyer profile | Investors / speculators | End-users, landlords, businesses |

| Observed uplift | ~20–40% over the period | To be established post-legislation |

| Key node | Chakri (M-2 access), Adiala | Ring Road industrial feeder belt |

Indicative Timeline to Watch

- Now: PIEDMC estate approved; Ring Road interchanges operational.

- Next: Punjab Assembly enabling legislation for the estate.

- Then: Land acquisition begins; plot allocation to industrial investors.

- Later: Construction, first operations, and the employment-led housing demand that follows.

How to Play It Without Getting Burned

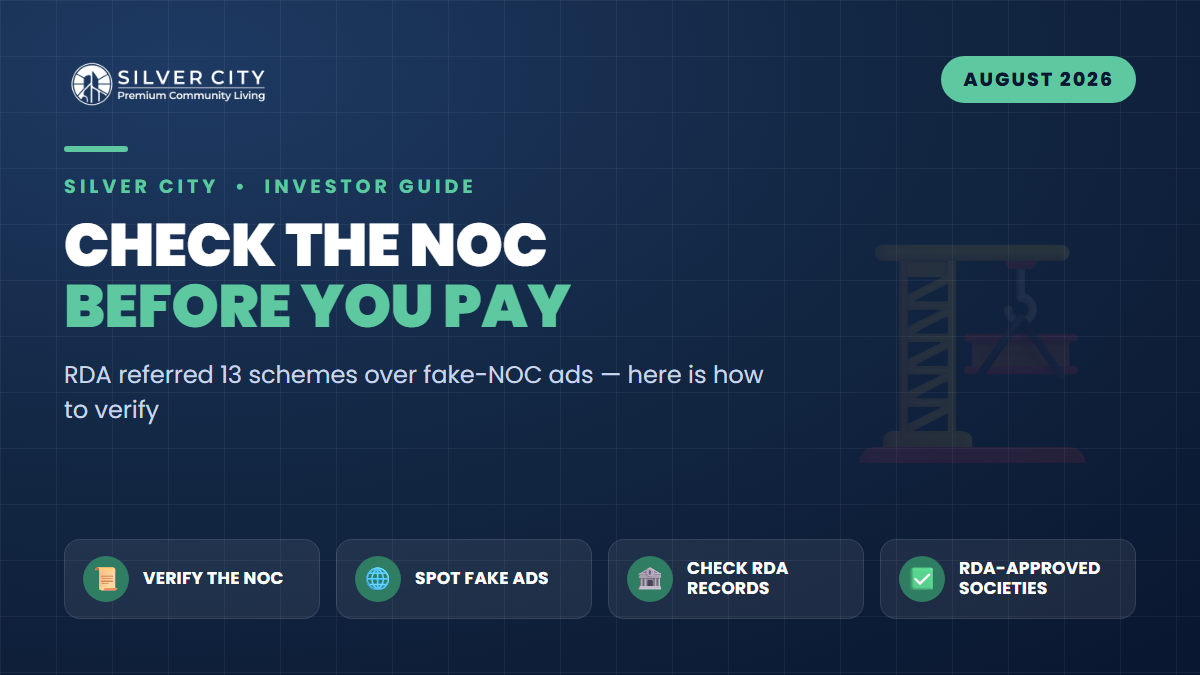

The opportunity is genuine, but the biggest risk in this belt is not the market — it is approval status. Several societies in the Chakri and Adiala belts carry disputed or incomplete approvals. Before you price in any Ring Road or CPEC upside:

- Verify the society independently through RDA (and CDA/PHATA where relevant). Never rely on a marketing brochure’s claim of “approved.”

- Prioritise interchange proximity. Plots with direct access to the Adiala or Chakri interchanges appreciate more than the corridor average.

- Buy the direction, not the hype. The estate is approved but not yet legislated — enter on fundamentals (approval, location, developer track record), and treat industrial upside as a bonus you did not overpay for.

- Think in end-user terms. Ask whether a future factory worker would rent or buy there. If yes, the demand base is real.

Frequently Asked Questions

Is the Ring Road industrial project a Special Economic Zone?

No. The original SEZ proposal was replaced by a PIEDMC industrial estate. Under Pakistan’s IMF programme, SEZ-style tax exemptions cannot be extended, so the estate model — which needs no such exemptions — was approved instead. It offers industrial land at affordable rates rather than tax holidays.

Can I buy a plot in the industrial estate today?

No. As of mid-2026 the Punjab Assembly has not passed the enabling legislation, land acquisition has not started, and no plots are open for application. Investors currently gain exposure through well-located, RDA-approved residential societies in the Adiala and Chakri corridors, not the estate itself.

Why does going from 7 to 44 SEZs matter for a plot buyer in Rawalpindi?

It signals that CPEC’s national focus has shifted from building roads to relocating and expanding industry. When that policy direction lands locally — as it has with the Ring Road industrial estate — it brings jobs and end-user housing demand, which historically produces more durable land-value gains than connectivity alone.

Which interchange is better for investment, Adiala or Chakri?

Chakri is generally rated higher because it connects directly to the M-2 Motorway and both cities, and hosts several high-end projects. Adiala anchors its own strong housing cluster. The better choice depends on your budget, the specific society’s approval status, and how close the plot sits to the interchange.

The Bottom Line

The next leg of value in Rawalpindi’s western belt will be written by factories, not just flyovers. CPEC 2.0’s pivot to industrial relocation, combined with the PIEDMC-approved estate on the Ring Road, sets up an employment-driven demand cycle around Adiala and Chakri — provided you buy verified land in the right location. Among the options in this corridor, Silver City stands out as an RDA-approved housing society worth serious consideration for investors who want to position ahead of the industrial shift while keeping approval risk off the table. As always, verify current status directly with the RDA before you commit.